Long Term Care Insurance

Insurance is a way to hedge your money.

The largest group of people who buy long term care insurance are the ones who have had personal experience. They've seen their mothers or fathers spend everything on care, the impact it had on them and their family, and they don't want that to happen to their spouse and children.

LTC Insurance is like health insurance, it's for really big events, the kind that could cause you to use up all your savings and assets.

People who haven't personally experienced or had to watch life savings disappear paying for long term care think that long term care insurance is expensive. The truth is that it's not cheap but still pennies on the dollar compared to the out-of-pocket cost of long term care.

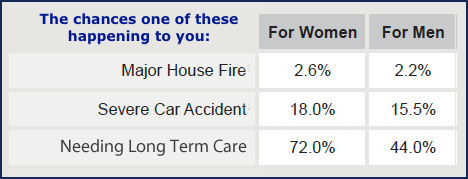

You have about a 3% chance of a major house fire and because of these odds homeowners insurance averages $1,100 a year. How much would homeowners insurance cost if the chances of your home being destroyed were 50% and how well would you sleep?

Because the odds are high that you and your spouse will need long term care, you should set aside an average of $250,000 each for care. That's $500,000 per couple.

Or you can buy insurance. Either way you have a good chance of needing care and either way you are going to pay for it: out-of-pocket or insurance. (source: longtermcare.gov)

Many people would say that house and car insurance are required, but long term care insurance is not.

1) The question then is would you buy house or car insurance if it wasn't required? Chances are you would not risk the cost of replacing your home or car out of pocket, but the majority of Americans do not insure for long term care and that puts many on the road to Medicaid.

2) Ask your house or car insurance agent how much a policy would cost with a 70% risk.

If you're the type that spends weeks or months looking into whether or not to buy long term care insurance and the horse gets out of the barn it's too late to close the door. You can't buy insurance after you need it.

Many have planned to self-insure. The same people would never self-insure a partking ticket that they could easiy afford, they put money in the parking meter to avoid the more costly ticket. Insurance is putting money in your long term care meter.

Who Should Not Buy Long Term Care Insurance

A long term care policy would not make sense for someone with low income and little or no assets.

You probably should not purchase long term care insurance:

- if you currently receive or may soon receive Medicaid benefits

- if you have limited income/assets and can't afford the premiums over the lifetime of your policy

- if your only source of income is a social security benefit or supplemental security income.

If you are considering replacing an old long term care insurance policy make sure the new policy is affordable because it will cost more since you are older. It should also have benefits that your old policy lacks.

Sometimes you would be better off keeping your old policy and adding a second policy to cover what is missing in your first policy. If you have questions about your current policy, we will be glad to go over what you have and provide you with your options.

Why People Buy Long Term Care Insurance

Here are six most common concerns about long term care and the reasons people buy long term care insurance:

- Burden - Do not want to be a financial or emotional burden on others.

- Access to quality care - Being able to select a quality facility in a location of my own choosing.

- Aversion to welfare (Medicaid) - Not wanting to be dependent on the government for care.

- Asset protection - Preserve assets for healthy spouse, inheritance for children or donation to charity.

- Control and independence - I want to maintain personal control in the choices I make.

- Peace of mind - Knowing I am protected instead of worrying about what could happen.

Do I Need Long Term Care Insurance?

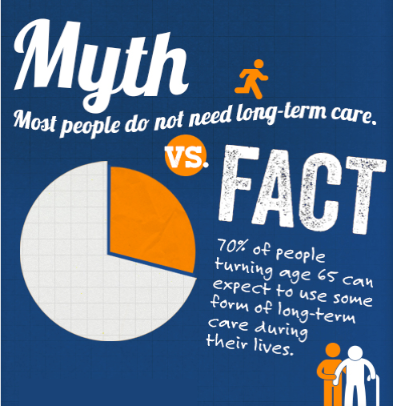

The majority of people are not aware of the likelihood of needing long term care.

The following questions can help you determine whether you may need the protection provided by long term care insurance:

1. Can you afford to use your savings or retirement income to pay for long term care at $150-$300 per day for 2-3 years?

2. Do you have assets excluding your home that are at risk?

3. Has anyone in your family ever needed long term care?

4. Would taking care of you be an emotional or physical hardship for your spouse/partner?

5. If your spouse/partner needed long term care, would you be able to provide it now and when you are older?

6. Would the people caring for you be able to maintain the quality of their own lives?

7. Are you concerned with being able to afford long term care?

If you answered "yes" to two or more of these questions you should consider long term care insurance.

Am I Too Old or Too Young For LTC Insurance?

Often what prevents people from insuring against the high cost of long term care is the cost of the premium.

Even though the younger you are the cheaper long term care insurance is, if you are older and can health qualify then long term care insurance will still be pennies on the dollar less than paying yourself.

If you are 45 years old and your policy costs $1,500/yr., and you paid for 30 years, that's $45,000. If you are 60 years old and your LTC policy cost $4,000/yr., and you paid for 12 years, that's $48,000.

If you paid for care yourself $48,000 would cover:

6-8 months skilled nursing home private room

10-12 months assisted living or memory care

12-14 months of home care

People who balk at paying $2,000-$5,000 a year for insurance are risking having to pay $5,000-$12,000 a month for care -- as Mr. Spock would say, "that's illogical."

What if you needed 4 years of care? Where would the $200,000+ come from?

The U.S. Government Accounting Office and The Wall St. Journal recently reported that as many as 72% of all Americans will require some long term care because we're living longer which makes needing long term care more likely.

Most LTC insurance policy buyers do not insure for the entire nursing home amount, usually 50%-80% with the idea of co-paying the difference if nursing home care is needed.

The logic is "If I'm in a nursing home I'm not going on any cruises, so I'll pay the difference between what the policy pays and the nursing home cost out of pocket, at least I'm not paying the entire nursing home cost." Most policyholders receive care at home or assisted living. See Claims

What If I Don't Qualify For LTC Insurance?

More people get turned down because of health reasons than for financial reasons. If someone doesn't health qualify they are now on the path to self-pay. See Are You Insurable?

But do not assume you cannot qualify. People who have had heart attacks, cancer, etc, some can still qualify. Get pre-qualified with a quote.

Applicants denied increases with age. |

|

| Age | % of those who apply and cannot health qualify |

Sometimes if one spouse cannot qualify for long term care insurance they both won't want the insurance. They are just reacting to the one spouses rejection.

How does that make sense? If one spouse loses their car insurance does the other spouse stop their car insurance? The situation is that if only one spouse can be insured then the money can be used for the non-insured spouses long term care.

Often if one spouse has insurance and the other doesn't and needs care they are very relieved that they have some protection. They might need all the money they have left after paying for care for the uninsured spouse to stay out of financial trouble.

Unlike many people who can't qualify for insurance you might be lucky enough to have the choice to either spend $200-$500 per month for insurance rather than $4,000-$9,000 a month for care.

Here is something that insurance companies wouldn't necessarily want you to know about or do. If one spouse has health issues that may disqualify them, you should be sure to indicate you are a couple when you apply. That way the spouse that is applying will still be able to get a partial couples discount.

With some companies “couples” can apply not only to spouses, but also to two people who meet criteria for living together in a committed relationship and sharing basic living expenses for at least 3 years.

"Considering that the average cost of nursing home care is approximately $70,000 a year, and home care costs can range from $50 to more than $200 a day, long term care insurance makes a lot of sense for millions of Americans."

- Chicago Tribune

How Much Does Long Term Care Insurance Cost?

Although it might be better to ask what could not having long term care insurance cost we do understand that everyone wants to know how much it will cost them to insure.

Since State requirements are different and each person is different the only way to know what your individual options are is to get a quote customized for your needs and preferences.

Premiums are based on your age, and two main benefit factors: the daily or monthly benefit amount and benefit term or years. If you have a health problem you may not be able to get insurance or may have to pay a higher premium.

Generally companies offer benefits ranging from $50 to $400 a day ($1500-$12,000/month) and benefit terms for 2, 3, 4, 6, years.

What to Look For in a Long Term Care Insurance Policy

A long term care insurance policy helps put you in control when you need it most - by helping to protect your assets and to ensure that you receive quality care in the setting you want. That's why it's so important to select a policy that's right for you.

A good plan design when judging policies is the National Association of Insurance Commissioners' (NAIC) model laws and regulations, which recommends:

* At least one year of nursing home or home health care coverage, including intermediate and custodial care. Nursing home or home health care benefits shouldn't be limited primarily to skilled care.

* Coverage for Alzheimer's disease.

* An inflation protection option.

* An "outline of coverage" that systematically describes the policy's benefits, limitations and exclusions, and lets you compare it with others.

* A guarantee that the policy cannot be canceled, non-renewed or otherwise terminated because you get older or suffer deterioration in your physical or mental health.

* The right to return the policy for a full premium refund within 30 days, if after having received the policy, you decide you don't want it.

* Options that enhance your policy such as Shared Benefits for couples, Home Care elimination period waiver.

* No requirements that policyholders first:

- Be hospitalized in order to receive nursing home benefits or home health care benefits.

- Receive skilled nursing home care before receiving intermediate or custodial nursing home care.

- Receive nursing home care before receiving benefits for home health care.

Also, be sure to consider the company behind the plan. Look at its track record in terms of experience in long term care insurance, as well as its ratings for financial stability and claims complaints.

That means you will need help with at least two of the six Activities of Daily Living (ADLs) for at least 90 consecutive days. These activities include bathing, dressing, eating, transferring, toileting and continence. You also are eligible for benefits if you are certified to need continual supervision due to a severe cognitive impairment.

When researching for a long term care insurance plan you want one that requires the insured to need help with only two (2) ADLs to trigger benefits for home, community, or nursing home care.

Some plans, especially group plans require the insured to need help with three (3) ADLs for nursing home benefits to be triggered. This means you may have to wait a lot longer before the insurance pays.

We will be glad to work with you to design a plan just for your needs. We have years of experience and work with the top long term care insurance companies.

Payment modes are pretty much the same for all companies. As with most insurances, the more frequently you pay the more it will cost per year.

Long Term Care is a family affair.

The majority of caregivers are family members.